The insured submitted a claim for water ingress due to a pipe burst that damaged 5 lifts.

Claim Stories

Claim Story #53 – Pipe burst damage to 5 units of lift

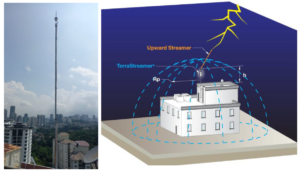

Claim Story #52 – Lightning Damage To Lift

Insured submitted a claim for damage to five lifts caused by a lightning strike.

The total claim submitted was RM96K++

The claim was approved but was subject to the Average Clause condition because the current Sum Insured for the building was considered inadequate.

The building’s sum insured has remained unchanged for the last 10 years; no valuation has been conducted.

As a result, the final claim amount recommended for approval was reduced from over RM96,000 to RM45,000 after applying the Average Clause due to the underinsured amount.

a) Construction costs including building materials, steel & labour increase annually due to inflation.

b) The sum insured of a building should be adjusted to reflect the nearest “reconstruction” or “reinstatement” This ensures that the building can be rebuilt to its original structure or condition.

c) Under the Strata Management Act 757:

d) It is the responsibility of the Joint Management Body (JMB) or Management Corporation (MC) to:

i. Ensure that the building’s sum insured is adequate;

ii. Conduct a valuation exercise at least once every five

e) Failing which, the claim amount may NOT be paid in full and will be subject to the average clause.

f) Any shortfall in repair costs and damages will need to be covered by the JMB’s account.

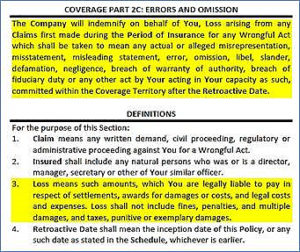

Claim Story #51 – Unit Owners Sue Management Coverage: Error and Omission

The insured submitted a claim for legal fees incurred while defending the management against allegations by unit owners. The dispute involved alleged misconduct relating to maintenance back charges and the sinking fund.

Claim Story #50 – Windstorm damaged trees

The insured submitted a claim for replanting and replacement of damaged trees.

Claim Story #49 – Water damage to electronic equipment

The insured submitted a claim for water leaking from the ceiling, causing damage to electronic equipment.

Claim Story #48 – Theft of Electrical Cables

The insured reported a theft of electrical cables belonging to a subcontractor at the work site.

Claim Story #47 – Fire Damage To Contract Materials

A contractor submitted a claim for material damages caused by a fire at the site storage.

Claim Story #46: Barrier Gate Faulty

A Joint Management Body (JMB) filed a claim for damages to:

– third-party vehicle; and

– the barrier gate.

caused by a malfunction in the barrier gate system.

Claim Story #45: Water Damage to 3rd Party Personal Contents

A Joint Management Body (JMB) filed a claim for damages to third-party property caused by overflowing discharge water.

Claims Story #44: No Actual Ignition or Fire

The insured submitted a claim for the replacement of a melted neutral cable.

Claims Story #43: Third-Party Bodily Injury and Property Damage

The insured submitted a third-party claim for bodily injuries and property damage to his bike after falling next to a road construction site.

Claims Story #42: Important of Fire Consequential Loss Coverage

A hotel suffered a fire incident, that damaged the hotel building structure & rooms.

Claims Story #41: CONTRACTORS ALL RISKS – CABLE THEFT

The insured submitted a claim for theft of cables.

Claims Story #40: WINDSTORM DAMAGES

We have received a claim for damages to the roof ceiling and 3rd party vehicle due to a windstorm.

Claims Story #39: ROOF STRUCTURE COLLAPSED

Received a claim for a roof structure that collapsed during construction.

Claims Story #38: CONSEQUENCES OF OVERSTATED CLAIM

The insured reported a flood at their warehouse.

Claims Story #37: Medical Claim NOT Payable?

Received a medical claim due to an Infected Penile Wound.

Claims Story #36: Fairness Claim Compensation

Condo Management sent a claim for damage to a neighbor’s wall caused by a falling tree.

Claims Story #35: The Importance of “Public Liability Insurance”

The Court of Appeal has upheld a lower court ruling that the management of a car park was liable for negligence, and ordered damages for a missing car.

Claims Story #34: Rat Bait Poisoning

Management received a claim from a unit owner for rat bait poisoning to his dog.

Claims Story #33: Damage to Drainage works – during maintenance period

Received a claim from an Infra contractor company for Drainage slope retaining wall collapse during the Defect Liability Period (DLP) / maintenance period.

Claims Story #32: House Bursting Water Pipes – Conceal inside the Wall

Received a claim for damage to a house unit caused by the bursting of concealed sewerage pipe.

Claims Story #31: Public Liability Claim – Bodily Injury ( Whose negligence? )

Received report from building management for an injury to 3rd party caused by the lift.

Claims Story #30: Risk Improvement for Lightning Arrester

A Condominium reported 5 lightning damage claims within a year period, resulted the claims ratio of more than 200%.

The existing insurer and others four (4) insurance companies refused to provide renewal quotation.

Before Risk Improvement:

After Risk Improvement:

Total claims amounting >RM50K per incident. The damage items were CCTV, Lift, intercom System & electrical parts.

All claims are payable with accumulation of more than RM100,000 ++

1. The important of Risk Improvement: –

a. To avoid similar incident from occurring;

b. To minimize unnecessary inconvenience or disturbance when any of the facility is not functioning.

c. To avoid additional work load and stressfulness in carrying out the repair work.

d. It helps to upkeep the value of the property.

2. With risk improvement, it could be helpful and in better position to convince the insurer to renew the policy with the same premium rate and terms.

3. Otherwise, no insurance company will cover the risk. They may impose additional premium loading and possibly with unfavorable insurable terms.

Claims Story #29: Bursting of Top Top Water Tank

Received a claim from a management corporation for water tank at roof top burst.

Claims Story #28: Extended Rooftop Damage By Cat’s Body Thrown Down

Received an enquiry from a condominium for a cracked extended rooftop caused by a cat’s body that was either thrown down by someone or the cat could have accidentally fell on its own.

Claims Story #27: Medical Claim Dispute (Medical Treatment Certification)

Received a claim for knee surgery known as “JOINTREP” for the implant treatment.

Claims Story #26: Falling Tree Damage to Property

Received a claim for damage property due to falling tree caused by strong wind.

Claims Story #25: Wall Collapsed Due to Soil Erosion

Received a claim for wall collapsed due to heavy windstorm, adjuster visited the site incident on the next day.

Claims Story #24: Amount Claimed vs Amount Approved

Received a claim from a Management Residence for damage to a 3rd party vehicle parked at the lobby due to impact from scaffolding.

")

Claims Story #23: Risk Improvement

Received a claim from a Condo for water meter pipe burst. The claim happened 2 months before policy renewal date. Total repair cost was about RM32k++.

")

Claims Story #22: Bursting Water Pipes – Damage to Lifts

A Condo Management reported of bursting water pipes at the pump room causing damage to four lifts.

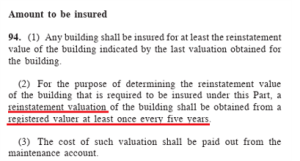

The Condo Management file claim for the four (4) lifts damages with repair quotation amounting to RM990K++.

Due to the huge amount, forensic expert from AGI (Approved Group International) was appointed for further investigation.

The policy was liable for the damages but more time was needed to finalize the case, due to the substantial claims amount submitted earlier.

The Claim was approved with the final amount of RM257++, reason for this claim was as follows:-

- Only essential replacement of damaged parts caused by the water was necessary.

- in most instances quite a number of parts does not need replacement but only servicing.

- not all parts were damaged by the water, only replacement parts for the actual damaged were approved.

- some items quoted were over prized.

1. Some lift vendors/contractors may offer unnecessary repair works and replacements.

2. The bigger value of claims will trigger more details of investigation.

3. The insurer needs longer time to finalize the claims, and it may cause delay.

4. Claim payment made must be fair and reasonable, as claim were payable to make good those item damaged and not meant to gain or profit from the claim submitted.

Claims Story #21: Damaged of Circuit Breaker – Speedy claim approval

Received a call from a condominium about a flashover that caused damage to the vacuum circuit breaker on Saturday morning.

Informed the Insurer immediately and Adjuster visited the incident site on the same day.

The incident resulted in the power supply being interrupted.

Claims Story #20 : Lightning Claim – Can repair bill be added on after the claim offer is out???

A claim was reported from a condominium about a damage to the card access system for the barrier gate caused by lightning.

Claims Story #19 : Student Sport Injury: Volleyball vs Skiing

Received a claim from an International School student who injured his right knee while paying volleyball.

The total submitted medical bills from various hospitals amounting to RM10K++.

The claim was rejected at first by the insurer. Reason being the injury sustained during the fall while playing volleyball aggravated the injury at the same location, where the student had met with an injury during a skiing incident in year 2019.

The Policy clearly stated that injury caused by skiing incident falls under the exclusion clause.

An appeal was sent to the insurer to have a further examine of the injury. Adjuster was appointed, an appointment arranged to have the student examine by an Orthopedic Consultant.

The appeal was successful and the claim was approved for RM6K++.

- Any reason(s) of rejecting a claim must be further scrutinize on its validity & the fairness of rejection.

- Not just simply and easily of accepting the reason(s) of rejection.

- It is the insured right to have a fair compensation and treatment.

- A responsible Agent will always be looking after the insured right and interest.

- Selection of a qualify agent is very crucial, they play an important role as when claim arises.

- The School has extended their appreciation to Dindings Corporate Insurance Agency (DCIA) as below: –

Claims Story #18 : Golfer – Hole In One

Insured reported of a golfer who fire a Hole in One in a game at a country golf club and the case was immediately registered with the insurer.

Claims Story #17 : Fire Damage to Condo Top Floor & Roof

Fire incident happened to a condominium penthouse and on the building roof top. The insurer was immediately be informed and adjuster visited site of incident on the same day.

Claims Story #16 : Stolen Cables at Construction Site

A M&E contractor submitted a claim for stolen cable at the site of a project.

Claims Story #15 : Water Damage to Outlet in Shopping Mall

A shopping mall was flooded due to the bursting water pipe and caused damages to all goods & fittings in few shops lots

Claims Story #14 : Stolen Cable in Project Site

A M&E Contractor reported a cable theft claim in a project site where the installed cable had been cut and stolen in all 15 floors inside the building.

Claims Story #13: Vacant Unit & Water Damage Claim

On 4th June 2020 neighbors complained of water leakage affecting few units, on 9th June adjuster visited the site of incident and discovered six units were affected and the cause was an overflow of sewerage pipe from unit 2A.

Claims Story #12: Insurance for Condominium

The Subsidence Landslip that occurred at a newly Condo due to heavy downfall, caused the damage to the water outlet and drainage system.

Claims Story #11: Contractor All Risks – Theft Case

OMG! Total stolen item worth RM150,000++

Claims Story #10: “Own Damage” or “3rd Party Vehicle Insurance”

Wah! How this happen?

A car suddenly knocked into the barrier gate while leaving a shopping mall. Luckily the driver escaped injury.

Claim Story #9: Public Liability

The Dog Vs. Joint Management Body (JMB)

A German Shepherd, lived at a condominium with his owner. Everything was peaceful, until one fine day the dog owner lost control, and the dog bite a visitor, a tuition teacher who suffered a torn pants

Claim Story #8: Error and Omission

A “PUPPY” Vs. Joint Management Body (JMB)

A puppy was kept by a tenant who stay in a condominium. JMB decided to take action, to advise her to move the dogs away from the Condo as this was against the Condo house rules. Excuses were given on why she insisted to keep the dogs, as it was a companion and part of her life and must be with her.

She engaged a lawyer to fight her rights and the case ended in the Tribunal Court. To defend the case, the JMB also engaged a lawyer for legal advices.

Verdict of the Tribunal Court, fined the dog owner of RM200.00 in favor of JMB.

The JMB file a claim for recovery of the legal fees incurred during the course of action.

Refer to the Error & Omission coverage terms: –

Firstly, there should be a proof of any “Wrongful Act” by the JMB. However, in this case there was none.

In addition, under the definition of loss it does not covers for legal costs in defend, as when the JMB is not liable.

The extract from the policy jacket: –

The Claims was rejected.

Majority of the Liability policy does not cover for legal fees. There are two versions of coverage terms provided by the insurers in the market, one with the inclusive of legal costs for defend, and the other is not. Of course, with the inclusion, the premium charged will be higher.

Claim Story #7: All Risks

Bursting Water Pipes – Damage to Lifts

On 6 Aug 2019 informed by a Condo Management Office of bursting water pipes at the pump room causing damage to four of their lifts.

We immediate notified the insurer to register the claim. The appointed adjuster visited the site of incident on the same day.

On 13 Aug 2019 the duly completed Claim Form and Incident Report were sent to the adjuster for processing together with a quotation of RM900k++. The condo management admitted that they didn’t review and negotiate, because they are not the “Lift Expert” and just leave it to the vendor and accept their proposal.

In view of the substantial claims amount, Approved Group International (AGI) was appointed as the forensic, to further assess on the damages.

Claim Story #6: Public Liability

A Resident’s Car Hit by Parking Barrier Gate

Received an accident report from a condominium management office, the car park barrier gate was malfunction and hit on a resident car. It caused the car front bonnet dented and paintwork was scratched. The car owner is claiming the damages from the JMB.

Claim Story #5: Public Liability

A Flying Object Hit on Student Forehead

It was raining heavily and the wind was strong. A student was walking back to the condo, as he passed the guardhouse, suddenly an unknown flying object hit his forehead and caused serious injury that needed at least 10 stiches. An incident report was raised by the condominium management office.

Claim Story #4: Burglary

Stolen Generator Set

This was a theft case happened in two blocks of Condo simultaneously. These two buildings were situated side by side. It was reported that the generator room was broken in and the key component of the generator set was dismantled.

Claim Story #3: Public Liability

A Shopper Fell Inside Toilet

While in the toilet of a shopping mall a shopper suddenly fell and suffered a broken bone. A complaint was lodged against the Mall Management for negligence as the floor was wet when she fell and claimed for compensation.

Claims Story #2: Combined Risks

Broken Glass Windows (Claim Settlement within 3 Hours)

Received a report from Condo Management for a broken glass window.

Claims Story #1: Goods in Transit

Cables Damaged During Transit

This is a cable manufacturer company. The company engaged a third-party transporter to deliver their finished products to their customer at Terengganu.

The cables were damaged during transit. The main cause was due to poor stacking and no proper tightening of the stocks on the lorry